Risky Business

The oil & gas business is RISKY and capital intensive, and most of the oilmen who survive have figured out how to use other people’s money to mitigate their risk.

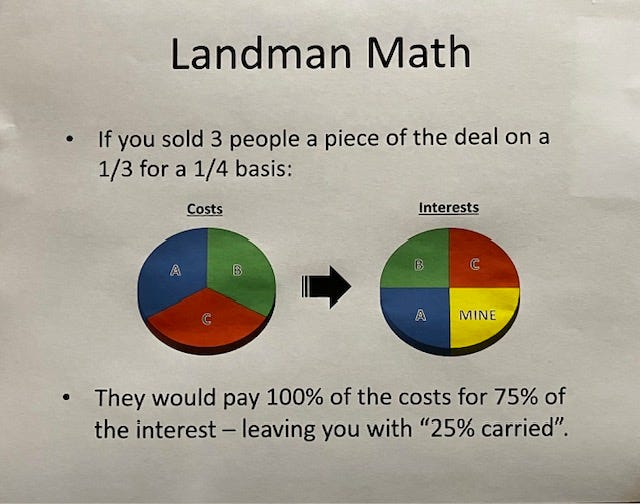

The classic deal structure that an operator would use to “promote” an investor to fund his oil & gas deal was referred to as “a third for a quarter.” In other words, the investor would pay for a third of all the costs for a quarter interest in the deal. So, if the operator sold his deal to three investors, they would collectively bear 100% of the risk for 75% interest, and the operator would retain a 25% “carried interest” – “carried interest” meaning that the investors paid for the operator’s share of the costs. With this deal structure, the operator effectively shifted all the risk to the investors by using their money to drill the well, while retaining a 25% interest if the well was successful.

It gets worse than that for the investors. The oil & gas lease will provide for a cost-free royalty to be paid to the mineral owner, which in today’s world is normally 25% of the oil & gas produced from the well, leaving the operator and his investors paying 100% of the costs and receiving only 75% of the revenues.

If we factor the royalty into this scenario, the three investors would pay 100% of the costs to drill and complete the well, then pay 75% of all future costs to produce the well, but would only receive 56% (75% x 75%) of the revenue.

To add insult to injury, the operator may also own the companies that service the drilling and production of the well, which means that he may also be making a profit on those services in addition to the 25% “carried interest” that he has retained in the well.

Just to be clear, the operator invested time and money putting his drilling deal together. At the very minimum, he paid a geologist to identify the prospective area and paid a landman to purchase the oil & gas leases to secure the prospect. So, in my opinion, the operator deserves to make a profit on his investment. However, it is up to the investor to make an independent assessment of the risk and determine if he has a reasonable chance to make a profit on his investment.

Bottom line – Neophyte investors in oil & gas deals may have a better chance making money on a craps table in Vegas – but the upside is that they can tell all their buddies at the country club that they were in the oil & gas business! Caveat Emptor!!

Let’s Make a Deal

As a Landman, part of my job was negotiating deals and getting the details of the deal put on paper. The two things that I learned pretty fast were: 1) after a verbal negotiation, everyone walked away from the table with a different interpretation of the deal; and 2) the “handshake deal” was a relic of the past, if it ever existed at all – a verbal deal changed until it was papered and signed by all the parties, and even then there was a good chance that it would be renegotiated. That’s why I became very interested in the “farmout” deal in Landmannegotiated by Monty and Diamond during their lunch meeting at the club. So, this was my interpretation of their deal and how it changed over time…

First, let’s define a few terms used in their deal:

Farmout: An oil & gas contract in which the owner of an oil & gas lease “Farmor” agrees to assign all or part of his interest in the oil & gas leases to the “Farmee” when the Farmee completes the obligations specified in the contract.

Drill to Earn: under a drill to earn farmout, the Farmee earns an interest in the oil & gas leases after he has drilled the well to a specified depth, regardless of whether the well results in a dry hole or a producer. This should be contrasted with a “Produce to Earn” farmout in which the well must be capable of producing oil & gas before the Farmee would earn an interest in the oil & gas leases.

The Handshake Deal – Episode #7

During lunch, Diamond told Monty that he had drilled six exploratory wells on the oil & gas leases in their prospect located in the Val Verde Basin, and four of the six wells resulted in producers (67% success ratio) that averaged over 200 barrels/day, and there was potential to drill 250 to 300 wells on the lease. He went on to acknowledge that he didn’t have the financing to develop his prospect, so he offered to farmout the oil & gas leases to Monty if he would agree to drill 54 wells on a “drill to earn” basis, and they would split the deal 60/40, with 60% going to Monty. Then he quickly backed down and said that he would go to 65%. After Monty discussed the deal with Tommy over the phone, Monty came back to the table with a counteroffer:

Monty would agree to pay 100% of the costs to drill and complete the wells on a “drill to earn” basis; however, Monty would receive 100% of the revenues from the wells, and upon recoupment of his investment (“payout”), his interest would be reduced to 70% for a twelve-month period and then reduce to 65% for the remainder of term. Diamond accepted the deal, and they shook hands to seal the deal.

My Comments:

1. The Val Verde Basin is located on the southeastern end of the Permian Basin and the wells in the Val Verde Basin have historically been gas producers. That doesn’t mean there couldn’t be a large oil play in the Val Verde Basin, but it would seem to be less likely than if they were drilling in the Midland Basin or the Delaware Basin, which are the Permian Basin’s most active oil producing sub basins (see map below).

2. I would assume Diamond’s exploratory wells were vertical wells, since initial production rates from a horizontal well that averaged 200 barrels/day would be considered very poor, if not uneconomic. On the other hand, an average of 200 barrels/day from a vertical well might provide “hope” that the production rate could be increased dramatically by drilling horizontal wells in the prospect.

3. Unless Monty was already intimately familiar with the geology of Diamond’s prospective area, I would’ve expected him to review all of Diamond’s geologic maps and other technical data before he would even consider making a deal. But this was just a TV show, so they probably didn’t want to bore the audience with a bunch of technical details.

When Did the Deal Change?

In Episode #10, we found Monty on his death bed, while his attorney met with Tommy and Monty’s wife, Cami (Demi Moore), to explain that Monty’s will provided for Tommy to assume the role of president of M-Tex, and that Tommy’s first order of business would be to make the decision to either sell the company or roll the dice and commit to the farmout agreement with Diamond.

Tommy and Cami met outside of the hospital to discuss the terms of the farmout, and this is how Tommy described the deal:

1. It would be a drill-to-earn farmout with a 54 well drilling commitment, with an upside potential of drilling 250 to 300 wells. The drilling commitment would require $167 million (that would equate to approximately $3 million/well, which didn’t make sense unless they planned to drill vertical wells).

2. M-Tex would pay 100% of the cost to drill and complete the 54 well commitment, and they would recoup 100% of their expenses from the revenues resulting from the successful wells, when they recouped their expenses, it would be reduced to an 80/20 split and settle at a 65/35 split. (Note that the handshake deal had the interest reduce to a 70/30 split for twelve months, at which time it would settle at a 65/35 split – when did the deal change?)

3. Tommy mentioned that the wells would be drilled to the Wolfcamp formation (which has been the primary target formation for horizontal wells in the Permian Basin since 2014), and that they would need a 65% “strike” (success ratio) to succeed, which was about the success ratio experienced by Diamond when he hit on 4 out of 9 exploratory wells.

4. Tommy also advised Cami that the upside could be $1.2 billion in 48 months, but if oil dropped below $60/barrel it would put them out of business.

It's All Talk Until It’s In Writing…

Tommy decided that Rebecca, the young big-city lawyer, would renegotiate the verbal farmout deal and that Nate, the old-time lawyer, would paper the final deal when Rebecca completed the renegotiation. He met his team at a location in the oilfield to discuss the new deal:

1. They would be drilling 10,000’ deep horizontal wells that would cost between $11 million to $18 million to drill and complete each well.

2. They would have an initial 9 well commitment, and if they hit on 4 of the first 9, then they would be obligated to drill 9 more wells, and if they hit on 4 of the second 9, then they would be obligated to drill 9 more wells… until the obligation reached 54 wells. He expected the initial 9 well commitment to cost $162 million (which equates to $18 million per well).

3. They would pay for 100% of the costs to drill and complete the obligation wells, and they would recoup 120% of their expenses from the revenues resulting from the successful wells before they started revenue sharing with Diamond. (Note that he changed the recoupment from 100% to 120% of expenses, and he didn’t elaborate on the subsequent percentage of revenue sharing, so it’s uncertain if that was also to be renegotiated.)

The best part of the meeting came when Tommy explained how they would drill the horizontal wells and then FRAC the wells to get them to produce. Suddenly the young “tiger shark” attorney showed her true colors as she got weak in the knees and said that she wasn’t sure she could negotiate a deal that involved the evil FRAC word. That’s when Tommy had to ‘splan the facts of life to the youngster:

“Good and bad don’t factor into this, Rebecca. Our great-grandparents built the world that runs on this shit right here. Until it starts running on something else, we gotta feed it or the world stops. There is an alternative. You can throw your phone away and trade that Mercedes for a bicycle or a horse and start hunting for your own food… But you’ll be the only one, and it won’t make a damn bit of difference. Plus, I hear the moral high ground gets real windy at night.”

Amen

Postscript

I can’t wait to see how Rebecca renegotiates the terms of the farmout agreement – that is if she doesn’t “throw her phone away and trade her Mercedes for a bicycle…”

If you recall, Tommy advised Cami that the downside of the farmout agreement was “if oil dropped below $60/barrel it would put them out of business.”

The price of oil is currently $72.50/barrel in the Permian Basin; however, if you’ve been listening to President Trump, then you’ve heard that he would like to see the price of oil at $45/barrel to help reduce inflation and stimulate the economy. In fact, Trump has said that he planned to meet with Saudi to get them to produce more oil so the price of oil would drop to $45/barrel. I’ll go out on a limb and predict that if the price of oil dropped to $45/barrel for an extended period of time, there would be no “Drill, Baby, Drill” and the next season of Landman would be about surviving the Oil Bust.

Like I said, it’s a Risky Business!

See you next season…

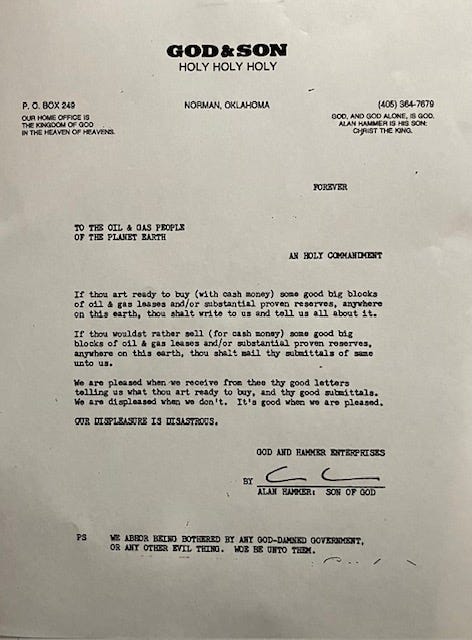

Let’s end with a good laugh…

While I was working, I would receive submittals for oil & gas deals all the time, most of them ended up in the circular file by my desk, but this one I kept for posterity…

The End

If you enjoyed my story, please hit the “Like” button and tell a friend about Let Me Tell You A Story.

Your comments, critiques, and questions are welcome, as always. Hit the Comment button below or email me at roger.beachbum@gmail.com

Please feel free to share my story with friends, family or any “neophyte investors” that you might know. Hit the Share button below.

Very interesting!